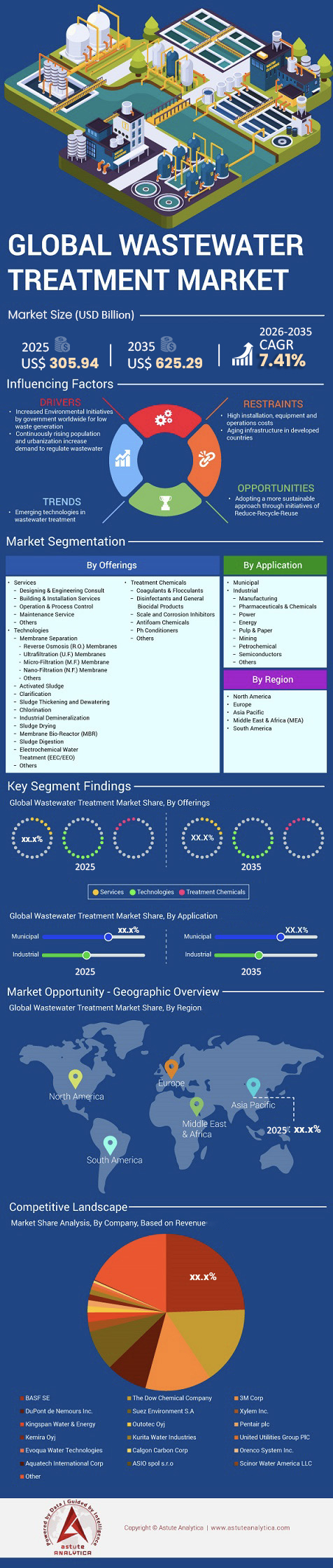

Market Scenario

Wastewater treatment market is anticipated was valued at US$ 305.94 billion in 2025 and is projected to surpass the valuation of US$ 625.29 billion by 2035, at a CAGR of 7.41% during the forecast period of 2026–2035.

Key Market Findings

- Based on offerings, technologies are expected to dominate the market with 68% of the market share

- By usage, municipal segment is expected to account for more than 62.12% of the industry share.

- North America leads the market with over 38.50% market share.

Global demand for wastewater treatment is intensifying amid rising water scarcity and regulatory enforcement. According to UN-Water (2024), the world produces approximately 268 billion cubic meters of domestic wastewater annually, yet 42%—over 113 billion m³—remains untreated, contaminating freshwater reserves and endangering public health. Treatment coverage varies sharply by income level, with 74% of wastewater processed in high-income countries compared to just 4% in low-income regions. Industrial treatment rates are even lower, with only 38% treated globally, underscoring a substantial infrastructure gap.

Asia-Pacific represents the epicenter of this challenge in wastewater treatment market. India still releases 62% of its sewage untreated, while rapid industrialization in China and Southeast Asia significantly increases effluent volumes. The pressure is compounded by urban expansion—by 2025, half of the global population will live in water-stressed areas, generating an estimated 359 billion m³ of total wastewater each year. Policy responses are rapidly reshaping the market: the U.S. PFAS drinking water standards (2024) affect 66,000 utilities, and the EU Urban Wastewater Directive revision mandates 80% micropollutant removal by 2045. These factors, combined with a USD 378 billion global project pipeline, are driving accelerated adoption of advanced treatment systems such as MBR, RO, and PFAS-specific filtration technologies.

To Get more Insights, Request A Free Sample

How Do New EPA Rules and Global Health Statistics Reshape Investment Strategies

The U.S. Environmental Protection Agency (EPA) finalized the National Primary Drinking Water Regulation in April 2024, setting enforceable Maximum Contaminant Levels (MCLs) at 4.0 parts per trillion (ppt) for both PFOA and PFOS in drinking water supplied by public systems. This applies to approximately 66,000 public water systems nationwide, with initial monitoring required within three years (by 2027) and full compliance by 2029 (potentially extended to 2031). These federal standards compel public and private water operators to monitor and treat PFAS contamination, shifting focus to advanced technologies for removal.

Meeting these safety standards is a global necessity given that untreated effluent contributes to 1.7 million deaths annually. Statistics indicate that over 80% of wastewater is currently discharged untreated worldwide, exacerbating the scarcity crisis in developing nations. Half of the global population will likely reside in water-stressed areas by 2025 without rapid intervention. The wastewater treatment market serves as a critical barrier against the pollution of natural aquifers and drinking sources. Therefore, expanding the footprint of secondary and tertiary filtration is essential for long-term health and security. Enhanced compliance strategies will redefine the economic landscape for every utility provider over the next five years.

Why Does High Tech Manufacturing Require Specialized Ultrapure Water Systems For Success

Industrial reshoring has placed immense pressure on local water supplies for high-tech manufacturing and chip fabrication. TSMC reported consuming 105 million cubic meters of water during 2024 operations to sustain its global production. Industry sources report 5,000–8,500 liters total water for processing a 300mm wafer, with ultrapure water (UPW) at 2,000–6,000 liters depending on fab efficiency and node (e.g., Veolia: 5,678L UPW; recent fabs: 2,000–3,000L). Modern plants recycle 70–90% via advanced treatment, reducing net demand.. Advanced 2-nanometer chip nodes commissioned in 2025 necessitate intricate 18-stage filtration loops to maintain product integrity. These precision requirements allow the wastewater treatment market to capture high-value industrial contracts across Arizona and Texas. Such systems utilize 4 distinct resin types within ion-exchange modules to ensure total conductivity removal.

Standard polishing loops for 2025 facilities maintain a 120 liters per second flow rate for constant cleanroom supply. Engineers target 1,000 Megohms-cm resistivity for high-grade effluent to remove every trace of organic and inorganic material. Global production reaches 359.4 billion cubic meters yearly, with 63% collected but only 52% successfully treated. Rapid urbanization surges these volumes, especially in the Asia Pacific region where industrial growth remains highest. The wastewater treatment market must scale significantly to accommodate the 22 new plants scheduled for 2025 completion. These facilities represent the peak of mechanical and chemical engineering within the current industrial landscape.

How are Advanced Membrane Specifications Setting New Efficiency Standards For Global Operators

Hardware innovation remains the cornerstone of filtration efficiency for industrial clients seeking long-term system reliability. Standard 8-inch reverse osmosis membranes now feature 440 square feet of active surface area for maximum throughput. Ultrafiltration units for 2025 utilize hollow fibers with 0.03 microns pore sizes to exclude bacteria and viruses. Recent PVDF membranes withstand up to 1,500 cleaning-in-place cycles before requiring total replacement. These specifications drive the wastewater treatment market toward longer asset lifespans and lower chemical consumption. Efficiency gains characterize the next generation of membrane hardware designed for high-salinity industrial loops.

Modern sequencing batch reactors and moving bed biofilm reactors achieve 80-90% efficiency in new Indian plants post-2018. Seawater reverse osmosis units achieved 99.8 salt rejection rates in 2024 tests, setting a new industry record. Hollow-fiber modules for 2025 utilize fibers with 0.5 millimeters in diameter to optimize the packing density. High-pressure housing units rated for 1,200 PSI enable deep brine concentration for zero-liquid discharge applications. Nanofiltration modules for textile dye recovery operate at 10 bar of pressure to isolate valuable pigments. These technical milestones allow for higher recovery rates in water-scarce regions within the wastewater treatment market.

Why is Zero Liquid Discharge Becoming The Standard For Brine Management Worldwide

Managing concentrated waste streams effectively remains a priority for desalination operators in water-stressed regions. Zero Liquid Discharge facilities recover 70 metric tons of salt daily in 2025 for industrial repurposing. Gulf reverse osmosis plants report brine discharge salinity at 45 parts per thousand in recent 2024 audits. Engineers install 5 energy recovery devices for every 10,000 m³ of capacity to lower electrical demand. These systems enable sustainable growth for coastal cities and massive industrial clusters. Brine management remains a critical pillar of the wastewater treatment market as reuse gains global traction.

Global daily desalination capacity reached 100,000,000 cubic meters during 2024 to meet rising urban demand. Planners expect 18 new mega-desalination plants to reach completion by late 2025 in the Saudi region. Marine protection standards mandate 0.8 millimeters maximum intake screen mesh sizes to protect local larvae. Industrial brine evaporators utilize 3 stages to achieve maximum concentration and high-quality distilled water return. Public sentiment identifies funding (27%) and awareness (23%) as key barriers to project implementation. Moreover, the wastewater treatment market ensures that concentrated discharge does not disrupt fragile marine food chains.

Will Massive Infrastructure Pipelines and Government Funding Accelerate Future Global Water Security

Infrastructure renewal projects demand durable materials and high-efficiency mechanical components for long-term survival. The NEOM project in Saudi Arabia will lay 1,200 kilometers of new pipelines by 2025. Standard municipal thermoplastic pipes now reach 60 inches in diameter for high-flow trunk sewers. California utilized treated effluent to irrigate 15,000 hectares of farmland in 2024 to combat drought. Energy needs dropped to 0.35 kWh per cubic meter for MBR tech in late 2024. Low-energy RO systems hit 0.22 kWh per cubic meter in 2025 using improved chemistry. The wastewater treatment market provides the backbone for these massive urbanization and irrigation projects.

A USD 378.2 billion global pipeline tracks water and sewage projects with 78.7% currently in execution. India’s Smart Cities Mission allocates INR 48,000 crores (USD 6 billion) for sewage plants by 2030. The AMRUT mission invests over INR 77,640 crores (USD 10 billion) for infrastructure upgrades. Plants use 40 variable frequency drives and 12 optical nitrate sensors for aeration per tank. US plants numbering 14,748 serve 238.2 million people but still face persistent infrastructure gaps. These investments ensure the wastewater treatment market can save 0.5 bar of pressure via fine-bubble diffusers. Subsequently, global water security depends on the successful completion of these high-capital projects.

Competitive Analysis: What Players are Holding Tight Grip on Key Waste Water Treatment Markets

Veolia, Xylem, Suez (Veolia), DuPont, and Evoqua command 60%+ of global wastewater treatment leadership, fueled by stringent PFAS rules and EU Urban Wastewater Directive revisions. North America holds ~38% market share, with U.S. Infrastructure Act channeling $21.4B to water SRFs and $10B PFAS remediation by 2029—driving DuPont's FilmTec Fortilife RO (>90% PFAS rejection) and Evoqua's Ionpure EDI into 66,000+ public systems. Europe mandates quaternary treatment for 80% micropollutants by 2045, boosting Veolia's Actiflo® clarifiers (500+ installs) and Xylem's Sanitaire® aerators in Germany's €47B upgrade pipeline.

Asia-Pacific grows fastest at 7%+ annually in the wastewater treatment market, as China's 100% urban sewage coverage deploys 4,000+ MBR units and India's Namami Gange adds 200 decentralized plants with $400M funding. Suez Aquavyst™ MBR and DuPont IntegraFlux™ UF penetrate high-density cities, while Permian Basin's 3.4M bbl/day produced water recycling favors Xylem Flygt pumps and Veolia Hubgrade® AI (140k users). Semiconductor fabs like TSMC demand 2,000–6,000L UPW/wafer, amplifying ZLD evaporators amid 22 new U.S./Asia reclamation plants by 2025.

Segmental Analysis

By offerings, Advanced Technology Offerings Secure Largest Value Share Within The Global Water Industry

Advanced technology offerings currently command 68% of the market share. Global Membrane Bioreactor installations surpassed 5,000 large-scale operational sites by late 2024. Consequently, tertiary treatment adoption included 1,200 new ozone disinfection systems commissioned during that year. Such technical growth remains evident as total worldwide desalination capacity reached 115 million cubic meters per day in early 2025. Furthermore, sludge-to-energy projects generated USD 1400 million in revenue from biogas recovery in 2024. Zero Liquid Discharge systems became mandatory for 800 textile manufacturing units in India, ensuring the Wastewater treatment market thrives through engineering innovation.

Industrial operators also deployed 3000 mobile treatment units for emergency water reuse. Simultaneously, membrane filtration technologies utilized 2.5 million square meters of polymeric sheets in 2024. Digital twin software monitors 1500 treatment facilities to prevent critical equipment downtime effectively. Beyond standard filtration, UV LED disinfection systems saw 400 new municipal pilots during the 2024 fiscal year. Advanced oxidation processes successfully removed 95 types of emerging contaminants in recent field tests. Such specific innovations reinforce the Wastewater treatment market as a leader in technical efficiency and chemical removal.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Application, Growing Municipal Infrastructure Requirements Lead Global Demand For Sustainable Water Management Solutions

The municipal segment currently accounts for more than 62.12% of the industry share. Urban sewage networks added 55000 kilometers of new piping across Southeast Asia in 2024. Meanwhile, North American utilities allocated USD 8000 million for aging infrastructure repair during 2025. European Union mandates require 2000 small towns to upgrade to secondary treatment levels. Public-private partnership models successfully funded 110 major metropolitan water projects last year. Such massive investments prove that the Wastewater treatment market relies heavily on government-backed expansion and modernization efforts.

Resource recovery remains central as municipalities recovered 1.2 million tons of phosphorus for agricultural use throughout 2024. Additionally, smart water meters are integrated into 15 million households to track effluent flow precisely. Recent combined sewer overflow events led to the construction of 40 giant underground storage tunnels. Global municipal wastewater discharge reached 360 billion cubic meters annually by late 2024. Water reclamation for urban parks utilized 25 billion cubic meters of treated effluent. Finally, sludge management costs reached USD 4500 million for metropolitan regions in 2024. Such budgetary allocations secure the Wastewater treatment market as a critical public utility pillar.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Maintains Market Supremacy Through Advanced Regulation and Infrastructure Reinvestment

North America currently leads the global wastewater treatment market, commanding roughly 38.5% of total market activity. Growth is driven by the U.S. Infrastructure Investment and Jobs Act, which allocates USD 11.7 billion each for clean water and wastewater revolving funds and USD 10 billion specifically for PFAS remediation.

Operators across the United States are prioritizing toxic substance removal and digital monitoring upgrades as facilities approach the end of their operational lifecycles. In the Permian Basin, produced water recycling capacity now exceeds 3.4 million barrels per day, reducing reliance on fresh aquifers.

Canada complements this leadership through a CAD 6 billion (USD 4.4 billion) commitment to improve water systems for First Nations and northern communities. Stringent EPA enforcement and advanced sensor technologies continue to underpin regional modernization efforts.

Asia Pacific Accelerates Global Expansion Through Rapid Urbanization and Industrialization

Asia Pacific remains the fastest-growing wastewater treatment market as China and India undergo accelerated urban expansion. China has achieved near-universal urban sewage coverage, supported by extensive installation of membrane bioreactor (MBR) systems across major cities. India’s Namami Gange and National River Conservation Plan programs together received approximately USD 400 million in new funding during 2025 for decentralized treatment installations along critical rivers. Across Southeast Asia, smart infrastructure projects are integrating real-time monitoring systems to detect leaks and pollutants, while rapid industrialization in Vietnam and Thailand has driven strong demand for on-site pretreatment solutions.

Europe Leads the Industry by Prioritizing Resource Recovery and Stringent Mandates

Europe remains an environmental leader in the wastewater treatment market, emphasizing resource recovery and energy neutrality in wastewater operations. The revised EU Urban Wastewater Treatment Directive mandates nutrient and micropollutant removal, prompting Germany to commit billions of euros for tertiary and quaternary upgrades. Over 1,600 biomethane facilities, many converting sewage sludge into renewable gas, now feed into European gas grids.

In the United Kingdom, multi-billion-pound investments are modernizing storm overflow and pipeline systems. High energy costs and emission targets continue to push European operators toward efficiency-focused, climate-aligned wastewater management models.

Top Recent Developments in the Wastewater Treatment Market

Top 7 Recent Wastewater Treatment Developments (2025 Company Announcements)

- Veolia (Jul 29, 2025): Launched Vitória WRS in Brazil—world's first large-scale municipal plant converted to water reuse via memDENSE™ MBR, ZeeWeed™ 500-EV UF, and PROflex™ RO.

- Veolia (Mar 18, 2025): Inaugurated Europe's largest primary settling unit at Seine Aval (34 m³/s capacity), treating wastewater for 6M Parisians with lamellar settlers, Energido™ heat recovery, and Predifloc™ optimization.

- DuPont (Aug 14, 2025): FilmTec™ Fortilife™ elements won BIG Sustainability Award for industrial MLD, enabling >90% PFAS rejection and resource recovery.

- DuPont (Jun 11, 2025): FilmTec™ RO/NF + IntegraTec™ UF won Global Water Awards' Industrial Project of Year at Foshan Jialida (China), recycling 3M m³/d water, saving 46.86M m³/year.

- Suez (Jun 14, 2025): Opened Eaux Blanches plant in Sète, France, for coastal wastewater recovery amid climate challenges.

- Suez (Apr 2, 2025): JV with Sonadezi (Vietnam) to upgrade Chau Duc Industrial Park wastewater for 100+ clients, adding cutting-edge O&M.

- Veolia (Sep 15, 2025): Secured Saudi Arabia's largest industrial water project for SATORP, maximizing wastewater reuse via advanced chain

Top Companies in the Wastewater Treatment Market:

- Suez Environnement S.A.

- Xylem, Inc.

- DuPont de Nemours, Inc.

- Evoqua Water Technologies Corporation

- 3M Company, Inc.

- Pentair plc

- United Utilities Group P.L.C.

- Kingspan Water & Energy

- The Dow Chemical Company

- Kemira Oyj

- Calgon Carbon Corporation

- Kurita Water Industries Ltd.

- Bio-Microbics, Inc.

- Trojan Technologies Inc.

- Aquatech International Corporation

- ASIO, spol. s r.o.

- Orenco Systems, Inc.

- Scinor Water America, L.L.C.

- Elgressy Engineering Services Ltd.

- Outotec Oyj

- BASF SE

- Blue Eden CleanTech Solutions Inc.

- Other Prominent Players

Market Segmentation Overview:

By Offerings

- Services

- Designing & Engineering Consult

- Building & Installation Services

- Operation & Process Control

- Maintenance Service

- Others

- Technologies

- Membrane Separation

- Reverse Osmosis (R.O.) Membranes

- Ultrafiltration (U.F.) Membranes

- Micro-Filtration (M.F.) Membrane

- Nano-Filtration (N.F.) Membrane

- Others

- Activated Sludge

- Clarification

- Sludge Thickening and Dewatering

- Chlorination

- Industrial Demineralization

- Sludge Drying

- Membrane Bioreactor (MBR)

- Sludge Digestion

- Electrochemical Water Treatment (EEC/ EEO)

- Others

- Treatment Chemicals

- Coagulants & Flocculants

- Disinfectants and General Biocidal Products

- Scale and Corrosion Inhibitors

- Antifoam Chemicals

- Ph Conditioners

- Others

By Application

- Municipal

- Industrial

- Manufacturing

- Pharmaceuticals and Chemicals

- Power

- Energy

- Pulp and Paper

- Mining

- Petrochemical

- Semiconductors

- Others

Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- Taiwan

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Brazil

- Argentina

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 305.94 Bn |

| Expected Revenue in 2035 | US$ 625.29 Bn |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Bn) |

| CAGR | 7.41% |

| Segments covered | By Offerings, By Application, By Region |

| Key Companies | Suez Environnement S.A., Xylem, Inc., DuPont de Nemours, Inc., Evoqua Water Technologies Corporation, 3M Company, Inc., Pentair plc, United Utilities Group P.L.C., Kingspan Water & Energy, The Dow Chemical Company, Kemira Oyj, Calgon Carbon Corporation, Kurita Water Industries Ltd., Bio-Microbics, Inc., Trojan Technologies Inc., Aquatech International Corporation, ASIO, spol. s r.o., Orenco Systems, Inc., Scinor Water America, L.L.C., Elgressy Engineering Services Ltd., Outotec Oyj, BASF SE, Blue Eden CleanTech Solutions Inc., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

The industry reached a valuation of USD 305.94 billion in 2025 and is positioned to surpass USD 625.29 billion by 2035. Projections indicate a consistent compound annual growth rate of 7.41% over the forecast period. Rapid industrialization and stricter environmental mandates remain the primary catalysts for this capital expansion.

Federal standards finalized in April 2024 established an enforceable limit of 4.0 parts per trillion for PFOA and PFOS. Compliance requires 66,000 public water systems to implement advanced sequestration technologies by 2029. Such a massive regulatory shift forces the market to prioritize high-rejection filtration and granular activated carbon solutions.

Logic chip fabrication requires between 2,000 and 6,000 liters of ultrapure water per 300mm wafer. Advanced 2-nanometer nodes commissioned in 2025 utilize 18-stage filtration loops to ensure total product integrity. These precision requirements allow the market to capture lucrative contracts for 22 new reclamation plants in the U.S. and Asia.

Modern facilities now recover 70 metric tons of salt daily and 1.2 million tons of phosphorus annually for industrial and agricultural reuse. Biogas recovery generated USD 1,400 million in revenue during 2024 alone. Circular economy models redefine the market by monetizing waste streams that were previously considered liabilities.

Smart facilities deploy 4,500 IoT sensors for every 100 MLD of capacity to provide real-time process visibility. AI-driven platforms like Veolia Hubgrade now support over 140,000 users in predicting equipment failures and optimizing chemical dosing. Digital twins generate 2 terabytes of monthly data, ensuring the market achieves maximum operational resilience.

Next-generation ultrafiltration units for 2025 feature 0.03-micron pore sizes to exclude pathogens with extreme precision. Modern PVDF membranes withstand 1,500 cleaning cycles, significantly extending the lifespan of filtration assets. These innovations allow the market to achieve a record 99.8% salt rejection rate in seawater desalination applications.

North America maintains a 38.5% share, but Asia-Pacific is the fastest-growing region with a 7% annual increase. China has deployed over 4,000 large-scale MBR units to achieve near-universal urban sewage coverage. India’s Smart Cities Mission allocates USD 6 billion for new plants, cementing the region as a primary engine for the wastewater treatment market through 2030.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |